Design Isn't Decoration. It's the Last Defensible Moat

In markets where functional performance has converged, the visible and experiential elements of a product become the only remaining competitive separation. Design isn't decoration. It's the last thing competitors can't easily replicate.

Australian firms filed 2,487 overseas design rights applications in 2024. A record, and a 7.8% increase year-on-year, according to IP Australia's 2026 report. They're not protecting how things look. They're protecting the last layer of differentiation that functional convergence can't erode.

The number matters because it reveals something most manufacturers, founders, and product teams still treat as secondary: design has become the primary vector for competitive differentiation in markets where performance specifications have reached practical equivalence across competing offerings.

Functional Parity Forces Strategic Pivot

Design protection extends well beyond aesthetics. It covers user experience, ergonomic refinement, and visible product differentiation, the aspects that influence purchase decisions when performance specifications have reached practical equivalence across competing offerings.

Economic research consistently demonstrates that as markets intensify in competition, firms shift emphasis from price-based strategies towards non-price dimensions of value. This manifests through heightened investment in design elements: appearance, tactile experience, interface logic, packaging presentation.

The pattern is particularly pronounced in mature product categories. Consumer electronics, household goods, and personal care products - sectors where functional innovation has reached diminishing returns now compete primarily on design-based modifications.

Design becomes protectable commercial infrastructure precisely when functional innovation stops delivering measurable advantage.

Geopolitical Competition Mapped Through IP Filing Patterns

The IP Australia data reveals distinct competitive methodologies playing out across identical consumer goods categories. US design filings increased substantially in 2024, with the increase concentrated in consumer goods classes. Chinese trade mark applications proliferated across the same categories during the same period.

Two approaches to market dominance emerge clearly:

Chinese manufacturers prioritise brand expansion and market presence. Industrial policies supporting cross-border e-commerce expansion have enabled accelerated product and brand proliferation since 2022. The strategy relies on trade mark protection—establishing brand recognition across numerous market segments simultaneously.

US firms protect product appearance and visible differentiation. Design rights applications concentrate in categories facing direct competition from Chinese manufacturers. The focus is appearance protection—creating defensible visual distinction when functional parity exists.

Two different approaches for how to win the same shelf. The divergence reflects distinct paths to competitive advantage: omnipresence versus perceived uniqueness. Brand velocity versus design protection.

Neither approach is inherently superior. Both respond rationally to market conditions and competitive threats. But the split reveals how IP filing patterns serve as proxy indicators for broader strategy — geopolitical commercial competition made visible through patent office data!

Australian Firms Pursuing Global Scale

Australian design applications grew across all five primary destination markets in 2024:

New Zealand: 35.8% growth (strongest increase)

United States: sustained growth in filings

China: continued expansion

United Kingdom: post-Brexit stabilisation

European Union Intellectual Property Office: sustained higher filing levels

The pattern suggests that Australian firms increasingly view the scale of our domestic market as insufficient to deliver a return on investment for their innovation. Record overseas filings indicate deliberate global commercialisation strategies and a recognition that design protection requires an international scope to deliver competitive advantage.

This isn't opportunistic expansion. It's a structural adjustment to market reality: innovation ROI now requires international scale from the outset, not domestic success followed by export consideration a decade later.

Post-Brexit Regulatory Fragmentation Creates Sustained Compliance Burden

Brexit created immediate filing surges in 2021 as firms navigated new requirements for separate UK and EU design registrations. Those levels have now stabilised—but at sustained higher rates, not temporary spikes.

The implication extends beyond UK-EU trade. Geopolitical fragmentation creates multiplicative compliance burdens for firms operating globally. Every regulatory separation requires duplicate filings, separate maintenance fees, and jurisdiction-specific monitoring.

This potentially favours larger organisations with resources to navigate complex multi-jurisdictional IP landscapes. Smaller innovators face disproportionate administrative overhead relative to commercial scale, a structural disadvantage that compounds as regulatory environments fragment further.

The trend suggests IP protection costs are becoming barriers to entry, not just operational expenses. Operations without dedicated IP infrastructure face mounting difficulty protecting designs across fragmented global markets.

Platform Economy Reshaping Product Competition

Whilst not explicitly stated in IP Australia's data, the rapid Chinese brand proliferation enabled by cross-border e-commerce points to fundamental shifts in how products compete.

Digital marketplace platforms - Amazon, Alibaba, Temu, and regional e-commerce systems have fundamentally altered the competitive landscape. Manufacturing excellence no longer guarantees market success. Brand velocity and design differentiation now determine visibility, conversion, and sustained market presence.

This creates distinct competitive dynamics:

Speed to market matters more than production optimisation. Firms that iterate designs rapidly and protect appearance gain an advantage over those perfecting single product versions.

Visual differentiation drives platform algorithm performance. Products that look distinct perform better in search results and recommendation engines than functionally superior but visually similar alternatives.

Brand proliferation becomes a viable strategy. Low barriers to market entry via e-commerce platforms enable rapid brand creation and testing protected through trade marks rather than design rights.

The shift isn't temporary. Platform economics rewards different competitive behaviours than traditional retail distribution does. Design protection becomes critical infrastructure for firms competing in platform-mediated markets.

Commodification Acceleration Across Mature Categories

The pronounced shift towards design-based differentiation signals that functional innovation is reaching diminishing returns across numerous product categories. Performance specifications have converged. Feature sets have reached practical parity. Manufacturing quality has been largely standardised.

What remains defensible? Visible, experiential, and aesthetic elements the aspects protected through design rights rather than patents.

This implies accelerating commodification, in which design becomes the last sustainable competitive moat. Firms that treat design as decoration rather than a strategic asset will find themselves competing purely on price, a race to the bottom that favours scale over innovation.

The pattern is already visible in consumer electronics, where functional specifications have largely converged and competition centres on appearance, interface design, and user experience. It's expanding into industrial products, medical devices, and commercial equipment - categories traditionally competing on performance rather than aesthetics.

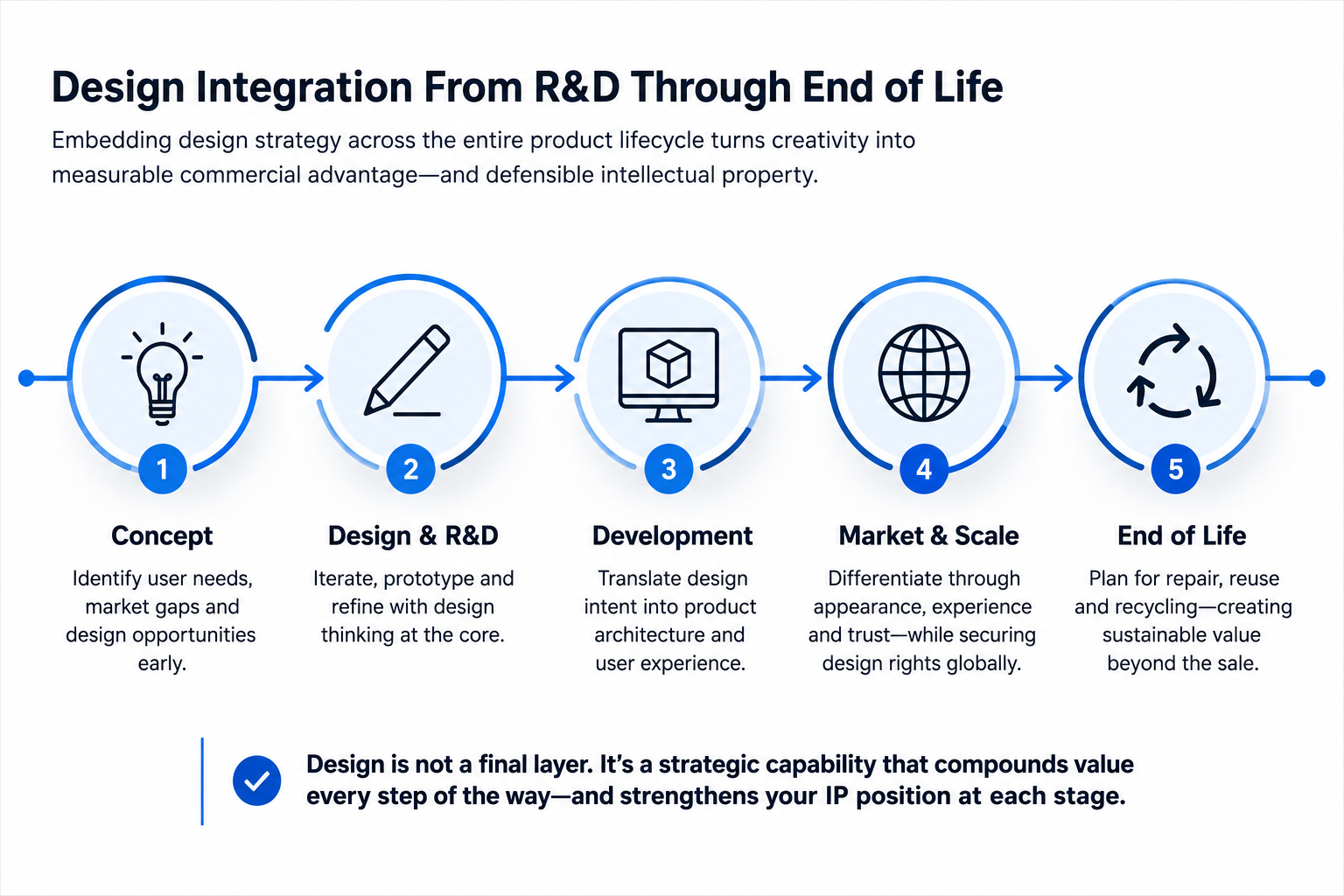

Design Integration From R&D Through End of Life

The evidence points to a clear structural imperative: design protection must be integrated into the commercialisation infrastructurefrom research and development through the product end of life. Not sequential. Not siloed. Continuous.

Most product teams still treat design as a late-stage cosmetic pass. Value proposition articulation is handed to marketing after the specifications are locked. Visual identity is bolted on before launch. By then, the protectable asset has already been diluted. A practical structure for embedding it looks like this:

At R&D concept stage, define the value proposition for each audience segment before the specs are locked in stone. Engineering choices then serve the proposition, not the other way around.

During prototyping, document design decisions that could qualify for registered protection - ergonomics, form, interface behaviour. Most of these opportunities are lost by launch.

Before commercialisation, file design rights in the jurisdictions where the product will actually compete. New Zealand filings grew 35.8% in 2024 for a reason. Domestic protection alone can leave a product exposed.

At launch, align the visual system, value articulation, and packaging with the protected design elements. The registered asset and the marketed asset should reinforce each other.

Throughout the product lifecycle, audit competitor filings on a cyclic basis. Design rights are territorial and time-limited, and gaps compound if left unmonitored.

At end of life, extract the design learnings into the next R&D cycle. Protected elements often carry forward. Unprotected ones get copied.

The organisations that embed this process, treating design protection as commercial infrastructure rather than finishing touches, are building competitive positions that functional parity can't dismantle.

What the Data Actually Reveals

Record Australian design filings overseas don't just indicate increased IP activity. They reveal strategic recognition that competitive advantage has shifted from what products do to how they appear, feel, and integrate into user experience.

The concentration of US design filings in consumer goods categories facing Chinese competition isn't defensive panic. It's a rational response to market conditions where functional parity exists, and visible differentiation becomes the primary competitive vector.

The sustained increase in post-Brexit UK filings isn't a temporary administrative adjustment. It's evidence that regulatory fragmentation creates permanent compliance burdens that favour firms with sophisticated IP infrastructure.

The data maps a fundamental transition: from competing on what you can build to competing on what you can protect. From innovation measured in functional specifications to innovation measured in defensible design elements.

Organisations still treating design as decoration, something addressed after technical product development, are competing with outdated assumptions about where competitive advantage actually resides in mature markets.

The operations that integrate design protection from R&D through commercialisation, that align value proposition articulation with visual differentiation strategy, that treat appearance as protectable commercial infrastructure - those are the ones building defensible competitive moats whilst other great Aussie businesses just commodify what they used to be good at.

Design isn't decoration. It's the last defensible advantage when everything else converges.

Written by Jeff Anderson, Founder of Arrow Strategic Communications.

Jeff leads strategy, software delivery, and workflow transformation initiatives across Australia.